2020 Q3 Review and Outlook

Keep Your Politics Out Of Your Portfolio

The stock market had a decent 3rd quarter, with the S&P 500 SPDR ETF (SPY) gaining 9.0%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) eked out a 0.4% gain, and a 60% stock/40% bond portfolio gained 5.6%.

Despite 2020 being…2020, investors have fared OK, with stocks returning 5.6% year to date (YTD), bonds 6.7% YTD and a 60/40 portfolio 7.8% (6.0% without rebalancing). Just to circle back from last quarter’s post, the benefits of rebalancing have increased as the year progressed. Not only did the YTD return from a rebalanced 60/40 portfolio exceed the unbalanced return by about 1.8% (or about $18,000 on a $1 million portfolio), the rebalanced portfolio return exceeded both the stock and bond portfolio’s individual returns.

To be fair, this does not happen all the time, and there are also other factors to consider, such as taking capital gains in taxable accounts. However, you can see how well it works when we get these sudden drops and spikes. The “problem” with rebalancing (and pretty much every aspect of investing) is psychology, as the optimal time to buy more stocks in 2020 was in March (“What are you kidding!? There’s a pandemic!”) and the time to trim your stock portfolio was in August (“Why do you want to sell when the economy is coming back?”)

Speaking of psychology…

In case you haven’t noticed, there is an election in November, and major elections magnify everyone’s fight or flight instincts. In our opinion, this has become much, much worse with the rise of social media platforms, which makes it even tougher to look at your portfolio and/or financial situation in a rational way.

We are starting to see these concerns bubble up from clients which have been expressed by: – 1) “Sell all of my stocks until after the election”; or 2) (If there is excess cash in the portfolio) “let’s hold off on investing until after the election.” Sometimes there is a political tone to the concern, as some clients believe that the country is going to collapse if Biden is elected/Trump is re-elected. Other times, clients are just concerned about “volatility.” They don’t want to wake up on the morning after the election and see stocks down by 20%.

We don’t blame our clients for feeling this way. Given the endless stream of headlines bombarding them daily – which has increased as people are stuck at home, watching the news or scrolling through Facebook or Twitter – the instinct is to dive for cover. Humans are built to detect threats. If we weren’t good at spotting trouble, we would have all been eaten by saber-toothed tigers long ago. The problem is that everything is a saber-toothed tiger right now, which makes it difficult to think rationally about portfolios that are designed to be invested over the span of decades.

How can you possibly fight all these huge hungry cats with sharp, pointy teeth? – stick to your plan. Why does something as boring as sticking to a plan work during elections? a) the volatility surrounding elections is very short-term in nature, and b) it doesn’t matter in the long term which party occupies the White House.

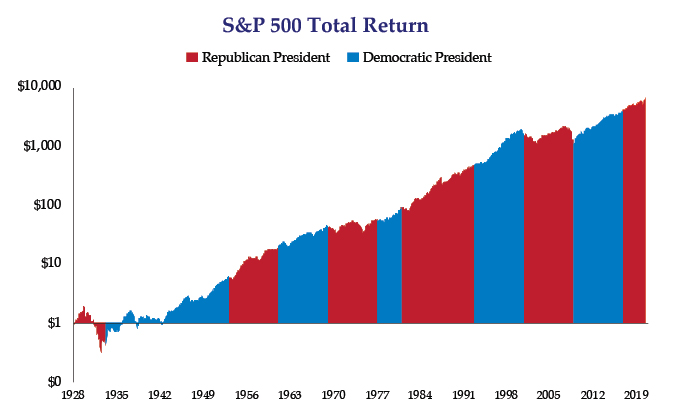

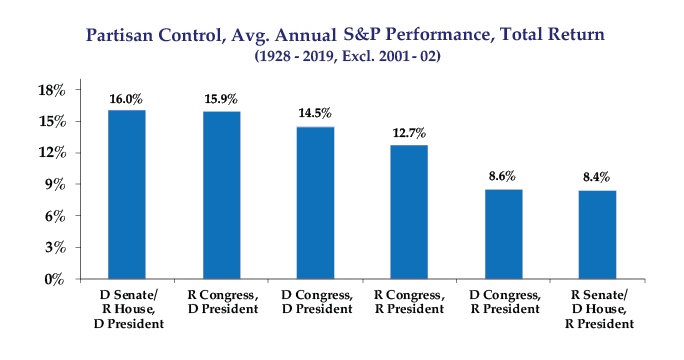

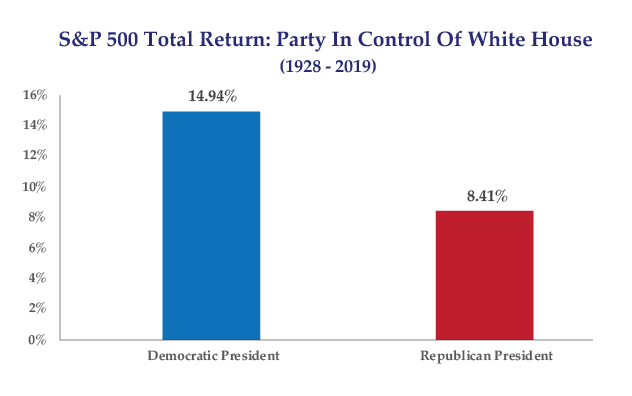

Probably the best data we can show to highlight how little Presidential elections matter in the long run is the historical return of the stock market by the party in the White House. As the following chart shows, there is not much of a difference in stock market returns. It doesn’t seem to make sense, but it does when you think about a) how huge and complicated the global economy has become; and b) how little direct influence the President has on the economy.

It can be counterintuitive as well. While the Reagan “it’s morning in America” administration presided over a huge bull market in the 1980s, Bill Clinton pushed through an income tax increase and had the best annualized stock market performance of any president since Calvin Coolidge. The annualized stock market return during the Obama administration was actually slightly higher than the Trump administration – even if you exclude the time period from COVID-19. This is not a political opinion – it just shows that uncontrollable and unpredictable forces are at work that are largely out of reach of even the most powerful person in the world.

Also, as 2020 has shown so starkly, the stock market is not the economy. It just reflects future expectations of corporate profits – which constantly change based on events that may or may not happen. A president can take all the “right” actions from an economic standpoint without any reaction from the market, and vice-versa.

With all that said, here is our guide on how to handle your portfolio in the context of the upcoming election.

1) Don’t have short-term money in long-term investments. If you have a known lump-sum expense coming up soon (e.g. $200,000 for a house down payment in 6 months), then by all means don’t have it in stocks. That goes for anytime, not just the eve of an election. Stocks are outstanding long-term investments, but they cannot be relied upon for short-term needs.

2) Don’t try to “time” the election. The market will probably do the opposite of what you think in the wake of the election, and trying to buy and sell based on your instincts and hunches will only throw off your overall financial plan. There are investors who sold their stocks when Obama was elected in 2008 and didn’t get back in until Trump was elected, foregoing a 190% gain in the process. Likewise, there are investors who sold everything when Trump was elected, and also missed out on healthy gains.

3) Use volatility as your friend. If the 2020 election is anything like the 2016 election, markets are going to be jumpy. Assuming your overall asset allocation fits your long-term financial plan, you can take advantage of rebalancing opportunities. If stocks skyrocket on November 4th and your 60/40 asset allocation goes to 65/35, then it might be a good time to trim that stock position. Likewise, if the stocks plummet and you are at 55/45, then take the opportunity to buy some stocks.

4) Go vote! By all means, vote for your preferred candidate. Just don’t expect the market to react in a predictable way.

Other than the election, what are we looking at now?

1) Progress on the economy. We are going to add one more letter to our economic alphabet – the “K” shape. In previous updates, we described the different paths for economic recovery in letters – L, U, W, V, from worst to best. The K has been in the news recently, and it makes enough sense to be worthy of consideration, even if the ultimate effects are unknown. In a K-shaped recovery, one part of the economy – the part that is best equipped to weather all of the recent shutdowns – rebounds quickly, while the other part languishes. The politically charged explanation is “the rich get richer and the poor get poorer,” although we believe it is more complicated than a simple headline. A New York City restaurant owner could have been classified as “rich” before COVID, but is probably struggling right now. Likewise, blue-collar electricians and landscapers have had a lot of business come their way, as people fix up the place where they are spending the most time – their home. As we have said, the ultimate “letter” will probably be somewhere in the middle (and the stock market will probably do something different.)

2) COVID-19. Progress on preventing and/or treating COVID-19 has come in fits and starts, with a multitude of vaccines and treatments in various stages of progress. The President even became an extremely high-profile test subject for an antibody treatment developed by Regeneron, which seems to have blunted the worst effects of the disease. Case count trends are different in every state (although mostly stable to down), and the economy continues to open bit by bit in a patchwork fashion. We would expect this slow progress to continue until a truly viable vaccine hits the market.

3) Government stimulus. The 2nd stimulus debate has reached a crescendo, with Pelosi, Mnuchin, McConnell and Trump all trying to get the upper hand before the election, although time is running out. We believe that everybody wants some sort of bill, but are still too far apart on the details. We continue to believe that there will be another round of stimulus (which should benefit the economy), but the ultimate form or timing is highly uncertain.

As we continue to say, none of this is predictable in the short term. The best action you can take in this environment is to review your overall long-term financial plan and adjust accordingly. A solid financial plan with an appropriate asset allocation, sensible investments and rebalancing as necessary will help you stay out of the noise of whatever happens to be blaring out of your TV or computer screen. So go vote, and we will see you after the election.

Charts Source: Strategas