2023 Q1 Review and Outlook – Silicon Valley Bank Stirs the Economic Pot

Financial markets had a positive but choppy start to 2023 as stocks (as measured by the S&P 500 SPDR ETF – SPY) gained 7.5% in the first quarter. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) returned 3.2%, and a 60% stock/40% bond portfolio returned 5.8%. Over the past 12 months, stocks returned -7.8%, bonds -4.6% and a 60/40 portfolio -6.5%.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Silly Valley Bank

We have been in the investment business a long time, so we think we’ve seen everything – and then another year goes by, and we are proven wrong again. At the end of last quarter’s update, we talked about “wild cards” – the risks that seemingly come out of nowhere and take the world by surprise. The thing about wild cards is that they generally don’t appear on people’s wild cards lists.

Last year it was Russia’s invasion of Ukraine. This year it was the near-overnight implosion of the 16th largest bank in the country – Silicon Valley Bank (SVB). Most people outside of the technology industry never heard of “Silly Valley Bank,” as analysts fondly referred to it. However, if you worked in or around the venture capital/startup space, SVB was everywhere. It did one thing extremely well – provide “soup to nuts” banking services to fast-growing venture funded companies. The bank made specialized loans to startups called “venture loans,” which are designed to bridge the gap between funding rounds. SVB charged high rates of interest and experienced very low defaults on these loans, which was very profitable. In addition to providing loans, SVB managed the cash of these companies. It had such great customer service and was so well-known in the venture community that pretty much everybody in the industry had deposits with SVB – most of which exceeded the $250,000 FDIC insurance limit (cue ominous music).

As the pandemic upended the world, the tech industry boomed. Venture capitalists raised huge funds and spent it quickly on startups that hoped to take advantage of the disruption hitting our working and living habits. SVB’s deposit growth surged as a lot of that venture capital money went straight onto SVB’s balance sheet.

This presented Silicon Valley Bank executives with a high-class problem – what do they do with all this money pouring in? They were limited on the amount of venture loans they could make, due to the high-risk nature of the borrowers. Furthermore, to offset the credit risk of the venture loans, they had to buy a lot of “low risk” bonds, such as treasuries and mortgage-backed securities (MBS). However, short-term treasury bonds yielded less than 0.2% in 2021. So, SVB committed one of the cardinal sins of investing – “reaching for yield.” In order to get even a 1% yield on treasuries or MBS in 2020-2021, an investor had to go far out on the maturity curve – 10 to 20 years. And that’s exactly what SVB’s Treasury department did. At the time, there was absolutely no concern about interest rate risk or liquidity, because deposits were coming in faster than they could be invested.

Of course, that all reversed in 2022.

Long-term treasury bond yields went from 1% to 4% in less than one year, which, as we discussed in previous updates, sharply decreased the market value of bond portfolios – especially portfolios with longer-term bonds. For Silicon Valley Bank, which had roughly a 7-8 year duration bond portfolio, that meant a 20%-30% decline in market value. Combine this with 10 to 1 leverage (which is normal for a bank) and you have a problem.

But, SVB’s managers had one last trick up their sleeves – they moved most of their bonds into a special accounting status called “held to maturity (HTM).” This allows the bank to carry the bonds at cost on its balance sheet until they mature. This is perfectly legal and is utilized by every bank and insurance company in the U.S. for a portion of their bond portfolios. However, there is a catch with HTM accounting. If even a single bond is sold from the HTM portfolio, then the entire HTM portfolio must immediately be valued at current prices not their costs. This is called “marked to market.” If SVB had done this, it would have been insolvent. But SVB’s executives relied on the fact that the bank had a supposedly loyal client base with “sticky” deposits, so the bank could ride out the bond market turmoil as their underwater bond portfolio slowly recovered and rolled off the books.

Avalanches often start with just a few little snowballs rolling down the hill, and, in 2022 venture funding slowed down as the tech industry was hit hard by the bear market. With less funding, the startup community burned more cash, which turned the huge deposit inflows into SVB into outflows. Silicon Valley Bank’s management saw the writing on the wall (as did the rating agencies, which warned them about a possible downgrade) and began to take measures to shore up their balance sheet with a stock offering. (Remember that they couldn’t touch their HTM bond portfolio to pay the withdrawals, and it was the vast majority of the bank’s assets.)

As it turned out, SVB probably had the worst deposit base in the world, because they all knew each other and were controlled by a small group of aggressive, fast-acting venture capitalists who also knew each other.

Once word of the stock offering made its way to the venture capital community, all hell broke loose. The venture capitalists panicked and told all their companies to pull cash out of SVB immediately. This was probably the largest bank run in his history and it was orchestrated via text message. $42 billion of withdrawal requests were made in one day. Given the speed of the bank run, the stock offering fell apart and the FDIC and Federal Reserve immediately stepped in and took over the bank. In addition, they also shut down two smaller banks (Signature Bank and Silvergate Bank) that were also teetering on the brink of insolvency with huge deposit outflows.

The Implications of the Banking Crisis

The speed of Silicon Valley Bank’s collapse was frightening, and investors and depositors naturally looked at the other 4,800 banks in the U.S. and wondered if it would happen to them. This wave of panic can be very unsettling – especially in the era of instant communication and bank apps on people’s phones that can be used to withdraw funds with the touch of a button.

Fortunately, we believe that the worst is behind us, for several reasons

1. Silicon Valley Bank was poorly managed. You’ve probably gathered by now that Silicon Valley Bank was not a typical bank. It had a concentrated customer base and egregiously bad risk management. While we believe that all banks currently have issues with underwater securities portfolios and deposit losses (especially regional banks that don’t have the extra “too big to fail” regulations of the money center banks), SVB’s issues were much worse. 2023 is going to be a difficult year for most regional banks, but – for the most part – their problems are solvable. SVB dug itself a hole it couldn’t climb out of (and their depositors quickly buried them).

2. The Federal Reserve took decisive action. Concurrently with the FDIC’s takeover of SVB, the Federal Reserve announced that it would extend a special facility that would lend against banks’ securities portfolios to help with liquidity in the case of skittish depositors. The Fed has always offered this service, but, in this case, the bank can borrow against the cost basis, not the market value of the securities. Given the unrealized losses in most banks’ portfolios, this provides a significantly larger source of emergency cash. The Federal Reserve/FDIC also announced that it would make SVB’s uninsured depositors whole, and implied (but did not confirm) that would be the case in the event of future bank failures. This particular decision was met with a lot of criticism as a “billionaire bailout,” and, strictly speaking, it was. However, most of the employees of these uninsured companies were not billionaires or even millionaires, and many would not have been paid their salaries at the end of the month had this action not been taken. What critics of the Fed/FDIC actions also miss is that the emergency measures were meant as a signal to every other depositor in the U.S. to not panic and pull their money out. No bank can withstand a bank run, and we believe that these “bailouts” helped prevent a much wider contagion.

3. Most banks have diverse deposit bases. Regardless of the government’s actions, we believe that the risk of a wider, national-scale bank run wasn’t quite as bad as the initial reaction. Remember that SVB’s depositors were all in the same network. It is hard to believe that we would see people lining up around the block of their local bank branch in St. Louis or Raleigh or Richmond, and that hasn’t happened, as far as we can tell.

That doesn’t mean that banks aren’t going to struggle this year. While we don’t expect massive bank runs, we do expect a steady outflow of bank deposits for a very rational reason – interest rates. Most people don’t give their bank deposits much thought, and banks know this and intentionally pay extremely low rates on checking and savings account balances. With the combination of 4%-5% short-term rates and the news coverage of SVB’s collapse, many people are starting to scrutinize their bank statements a little more closely, and some portion of those people are going to transfer those deposits into money market funds to earn a lot more on their cash. However, it’s a cumbersome process to switch financial institutions, and sometimes the bank will offer a higher rate and keep the customer. As a result, bank deposit flows should be more of a “slow bleed” than the “sucking chest wound” that some of the more panicked news outlets implied.

To be fair, we expect continued fallout among the weakest banks. After many near-death experiences over the past 20 years, Credit Suisse finally succumbed and sold itself for pennies on the dollar to its stronger Swiss rival UBS. Another west coast bank, First Republic (which had the same problem as SVB) is hanging on by a thread, with big banks such as J.P. Morgan pitching in cash to buy it time and calm the depositors while it runs off its underwater securities portfolio.

Regarding our bank investments, we own two bank stocks in our model portfolio. J.P. Morgan (JPM) should benefit from the recent crisis, as its strong balance sheet is very attractive to nervous depositors looking for safety. Our other bank, U.S. Bancorp (USB) will have some difficulty this year, but we believe that it has enough wiggle room in its balance sheet to get through this period and its strong brand in the Midwest should allow it come out the other side in good shape. We obviously will be watching the entire financial sector closely as events unfold and will act (either positive or negative) if necessary. As usual, we try to stay out of the short-term noise when evaluating investments, but we also want to avoid large unrecoverable losses in clients’ portfolios.

The “stuff” economy keeps slowing – the “people” economy keeps growing

The U.S. economy continues to trundle along at a slower and slower pace as the quarters go by. Almost every economic indicator is either barely growing or has flipped to contracting – especially when it comes to “stuff” (e.g., the Purchasing Managers Index surveys, Architectural Billings index, Federal Reserve regional economic reports, durable goods orders, housing starts, etc.) However, when it comes to “people,” the data is still mostly positive (e.g., unemployment, job openings, wage growth, etc.) This puts the Federal Reserve in a difficult position, and the latest interest rate decision was a “throw up our hands and split the difference” 25 basis point increase.

To be sure, we believe that the economy will continue to slow, and the “people” metrics will eventually catch up (catch down?) to the “stuff.” The bank deposit outflows will create yet another headwind, as the banks need those deposits to make loans. If deposits shrink, then – all else equal – loans will shrink, and this will reduce new business formation and real estate activity.

Speaking of real estate, the pressures of remote work are finally catching up to the commercial real estate (CRE) market, as office vacancies have risen dramatically and weaker and/or more aggressively financed properties have begun to default. As banks increase their reserves against future CRE losses, lending will be further restricted, which will also create another drag on economic activity.

Inflation

If there is a silver lining to the recent banking chaos, it could be on the inflation front, as a nationwide lending slowdown will literally take money out of the economy. Since the change in the money supply has a large impact on the future inflation rate, Silicon Valley Bank’s failure may have inadvertently solved the inflation problem.

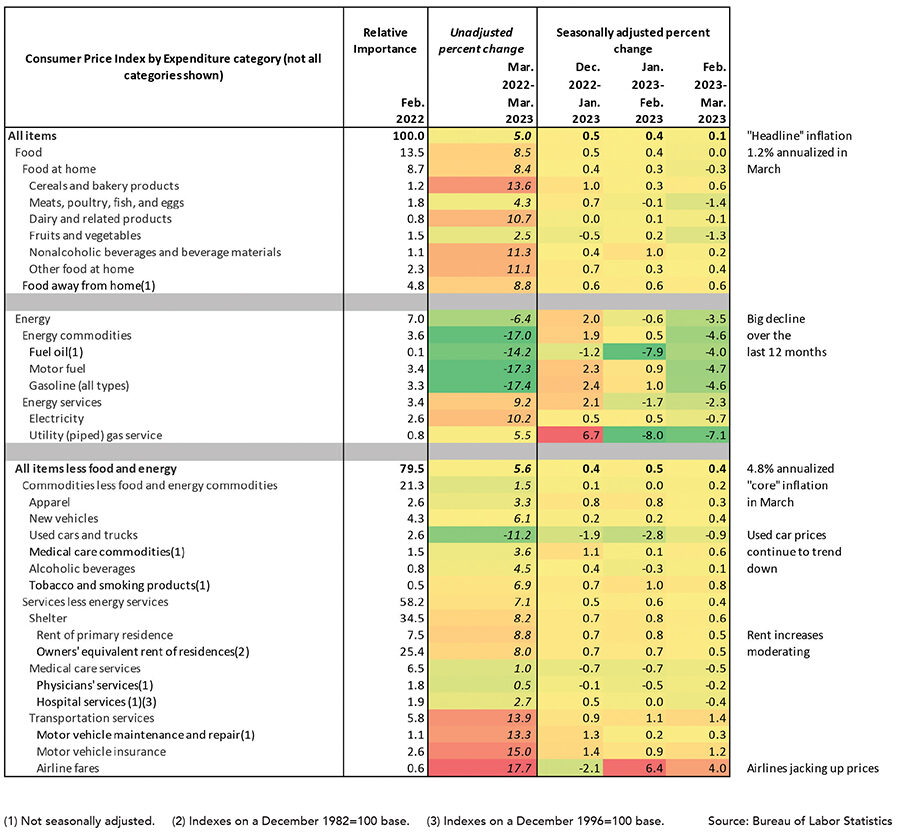

As the most recent inflation report showed, the inflation rate has already been slowly but steadily dropping. As figure 2 shows, the CPI increased only 0.1% from February to March (1.2% annualized) while the less-volatile “Core CPI” (i.e., CPI without food or energy costs) increased 0.4% (4.8% annualized). Year-over-year, CPI increased 5.0% and the Core CPI increased 5.6%. A large drop in energy prices (-6.4% year-over-year) certainly helped, while other factors such as rent (+8.8% year-over-year) have been harder to turn around. (Although judging by the number of new apartment complexes springing up in the Richmond area, rent increases may finally start to moderate.)

Will the Fed Pause?

With all that said, the writing is on the wall for the Fed to either a) continue with its smaller 25bps rate hikes or b) implement the long-awaited “pause” to allow the different pieces of the economy (which have been put in a blender over the past year) to settle down. Chairman Powell and the more hawkish members of the FOMC may point to continued Core CPI growth well above the 2% target and push for more hikes, but the expected decrease in bank lending coupled with the slowdown in “stuff” may push them over into the pause camp.

While the activities of the Federal Reserve undoubtedly have a large short-term influence on the markets, we prefer to stay out of the short-term noise and build our investment strategy around longer-term trends and – especially – the needs of a well-constructed financial plan. If the client absolutely needs every penny of their investment portfolio over the next ten years, then we are going to be conservative, regardless of whether some guy on CNBC says to “load up on stocks.” If the client is 30 years old and doesn’t have a lot of cash needs, then their portfolio will have a lot more stocks, even if the bearish economist on Fox News (who has probably predicted 15 out of the past 3 recessions) thinks stocks are going to crash next month. While we may make some adjustments to certain securities in the portfolio that may be better equipped to handle the current economic trends, the overall strategy doesn’t change because an economic report is 0.1% higher or lower than expectations.

We hope everyone has a great Spring, and please contact us if you have any questions.

Figure 2: Selected Components of the Consumer Price Index (CPI), March 2023