2024 Q2 Review and Outlook – A Market of (One) Stock

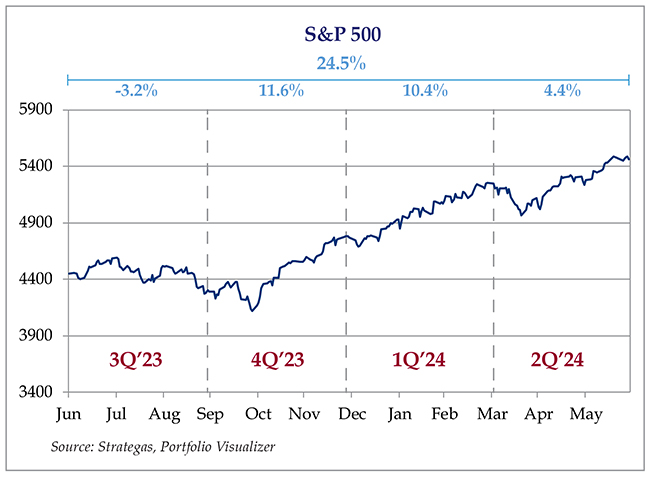

Markets continued to rise in the second quarter as stocks (as measured by the S&P 500 SPDR ETF – SPY) gained 4.4%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) was flat, and a 60% stock/40% bond portfolio recorded a 2.6% total return. Year to date, stocks returned 15.2%, bonds -0.7% and a 60/40 portfolio 8.9%. Not bad for six months’ work.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

NVIDIA – A Market of (One) Stock

Back in the day, when traditional stockbrokers were charging $250 per trade, they had a popular saying – “It’s not a ‘stock market’ it’s a ‘market of stocks,’” implying that you should be picking stocks and not buying an index. This saying was used a lot to get clients to pay for a LOT of $250 trades, putting their faith in their broker’s ability to find those hidden gems rather than simply buying a mutual fund. (It usually didn’t work out well for the client).

The current market conditions take this saying to the extreme.

We have written at length about how index returns have a lot more going under the surface than people appreciate. Although the S&P 500 is literally 503 stocks, they are weighted by market value. You can invest in an equally weighted version of the S&P 500 index (ticker: RSP), but most index fund investors have their money in “cap weighted indices.” From a theoretical perspective, it makes sense. If you were a zillionaire and wanted to buy the entire S&P 500 outright, you would need to invest a lot more money to buy the largest stocks vs. the smallest. Accordingly, if a large investor put billions of dollars into an equally weighted index, s/he would be buying a huge percentage of the smallest stocks, but a much smaller share of the largest. For mere mortals, this isn’t a problem, but if you consider all the investors in aggregate, it adds up. This is why cap weighted indexes are the most efficient way to own a basket of stocks.

However, some weird things can happen when a few very large stocks catch fire – they start to completely dominate the returns of the index. In the short to medium term, this can be a great thing for an index investor, and, to be honest, you could do worse than just automatically plopping a percentage of every paycheck into a handful of broad-based index funds and forget about it – especially if you are young. That being said, these distortions can create very unbalanced indices which depend on just a few massive stocks for future returns.

We have lived through “FAANG,” the “COVID stocks” and most recently the “Magnificent Seven.” The 2022 bear market cleaned out most of the FAANG and COVID stocks, and the Magnificent Seven is down to six. But one stock has completely taken over the market – NVIDIA (NVDA). NVIDIA makes high speed computer chips. Until last year, it was known for two products: a) high-end gaming computer graphics processors, and b) the key components for cryptocurrency miners. When the crypto market crashed, so did NVDA, and everyone wondered if the company would be able to grow again. Artificial Intelligence (AI) came to the rescue, as its chips are best suited to the intense computational requirements of writing high school term papers for kids who don’t want to study. Its profits took off, and the stock went with it, tripling over the past year, with a 40% increase in just the past three months.

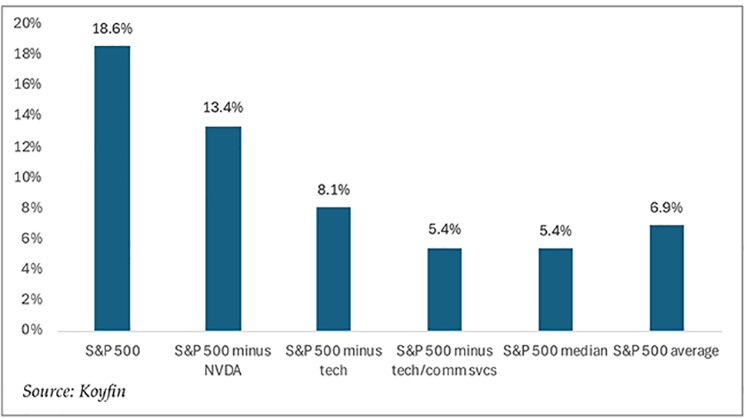

What does this mean for the index investor? In short, almost 30% of the year to date (YTD) returns of the S&P 500 can be attributed to NVDA stock. As of July 10, 2024, the S&P 500 is up 18.6%. Without NVDA the index would only be up 13.4%. Furthermore, the Technology and Communications Services sectors (which are the most influenced by the AI trend) contributed a combined 13.2% of the 18.6% return. That is 71% of the YTD total return.

While the index returned 18.6%, the average stock return (i.e., assuming equal weighting) was only 6.9%, and the return of the median stock (the 250th best performing stock) was only 5.4%.

Figure 2: Contribution to S&P 500 YTD total return as of 7/10/2024

Now, 18.6% is 18.6%, and we are very happy for S&P 500 investors. However, investors in the “boring” S&P 500 had better like technology and internet companies, because, for every $100 invested in SPY, $6.90 is invested in NVDA and $32 is invested in Microsoft, Apple, NVIDIA, Amazon, Meta (Facebook) and Google. The largest non-tech, non-internet stock is Berkshire Hathaway (BRK.B), at only 1.6% of the index.

We like the technology sector, and tech is by far the largest weight in our domestic large cap model portfolio. However, we aren’t sure about putting 7% of our stock portfolio in Apple or Microsoft or NVIDIA. When just a few companies have that much influence on portfolio returns, they must continue to go up, because they are carrying the index on their backs. This dominance may persist for another year or another five years, but it’s impossible to forecast when one or all of them will stumble. The result of a “stumble” will probably look a lot like 2022, which caused a lot of pain for investors.

On a positive note, this means that there are a lot of high-quality stocks out there that have been left behind by the AI craze and are still reasonably priced. That is encouraging when we read the headlines about how expensive the S&P 500 is right now. The “Magnificent Seven” might be expensive, but what about the “S&P 493?”

Inflation – Back on the Right Track

In another bit of good news, inflation seems to have lurched back into its lane after veering off course the previous quarter.

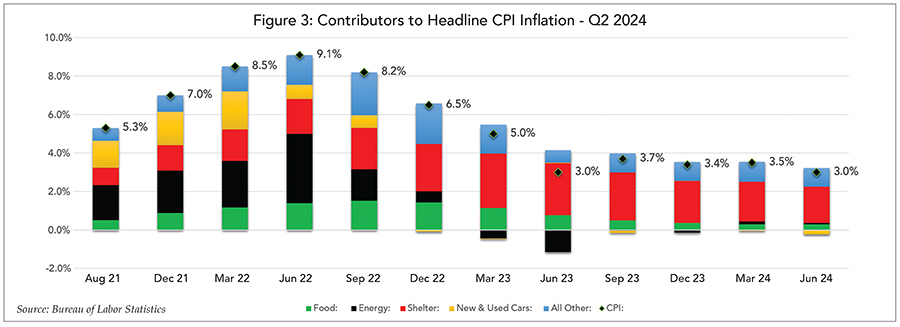

The year-over-year growth rate of the Consumer Price Index (CPI) dropped to 3.0% vs. 3.5% growth in March. The “Core CPI” index (which excludes food and energy and includes 80% of the CPI) followed the same trend and fell to 3.3% vs. 3.8% in March. Both measures were well below economists’ expectations – a very welcome sight after the alarming numbers in March. Shelter inflation continues to be the largest part of the CPI, contributing almost 2/3s of the total growth rate. However, even this sticky wicket has loosened since the end of 2022, and we are seeing some newly built apartment complexes struggle to fill their rooms. New and used car prices are now below the levels of 12 months ago, which reduced the CPI growth by 0.2 percentage points. Figure 3 breaks down the inflation reports since August 2021 by major CPI component.

However, we will make our first-grade teachers proud by pointing out that 3% is larger than 2%, and the Federal Reserve wants 2%. 2.000%, not “about 2%.” As we noted in last quarter’s update, the last bit is the hardest. The supply chains have unclogged, the spending boom from the COVID stimulus payments is mostly behind us and energy production has resumed. Removing one more percentage point may involve taking a little bite out of the economy, which could have unintended consequences and turn into a big bite.

Most economic indicators are showing signs of slowing, including the stubbornly strong ISM Services Index, which dipped into negative territory in April before rebounding in May. The Manufacturing Index has been negative for over a year. Retail sales and housing starts have also softened.

On the other hand, the Federal Reserve’s favorite inflation measure – Core Personal Consumption Expenditure (PCE) growth – is much lower than the CPI (about 2.5%). Plus, the consumer is slowing down but far from stopped. In fact, the TSA reported that July 7th was an all-time single-day record for passenger screenings. Finally, the unemployment rate continues to hover around an extremely low 4%, despite some moderating trends in hiring.

The Federal Reserve Open Market Committee meets at the end of July, so this new data will give them some food for thought as to the timing of a possible rate cut. After the poor inflation reports last quarter, a July cut was taken completely off the table by economists and “Fed watchers,” but it may have at least snuck back to the kid’s table for the next meeting. Nevertheless, a July cut would still be a surprise, and would probably send the stock market further upward. Most analysts will instead be focusing on the tone of Chairman Powell’s comments to see if a cut might happen in September rather than November.

Remember that Jerome Powell is laser-focused on the 2.0000% inflation target, and he has been successful in reeling in the more “dovish” members of the FOMC. We believe that he is willing to trade short-term growth for long term price stability, which could include a recession.

The Election

We wince at typing “election,” because the topic has become radioactive in recent years. However, it is an important event – one of the most important events in the world every four years.

It is also an important event to investors, although the perceived importance in terms of economic growth and stock market performance is much, much higher than the historical performance. Nonetheless, investors are humans who will become emotionally invested with the outcome, which then bleeds over into their financial investing process. It’s very natural to believe that your stock portfolio is going to skyrocket because “your guy” won the election and vice versa.

And recently, things are getting more chaotic following the recent presidential debate between Trump and Biden. Although President Biden insists he is going to continue as the Democratic candidate after a disastrous performance at the debate, he is still vulnerable to being replaced. This has created more uncertainty and strengthened Donald Trump’s hand, with polls in most swing states indicating a movement toward the red side. And, just to put a cherry on top of the craziness, we had the awful scene of the attempted assassination attempt on Mr. Trump over the weekend.

More uncertainty…more stress…more temptation to veer from your financial plan.

This doesn’t mean that you shouldn’t vote or express your political opinion. However, few people will be directly impacted by a new administration from an economic perspective. These few people would fall into the following categories:

- You are a federal government employee, or a state government employee that is tied closely to the federal government. Sometimes a new administration will “clean house” and put “their people” into place. They may also dramatically shrink or expand different departments.

- You work for a government contractor. Shifting political priorities could mean cutting long-term “safe” contracts or expanding contracts.

- You work for a company that either receives government subsidies or has a customer base that receives government subsidies for purchasing your product. This includes companies in many sectors, some of which would be unprofitable without direct or indirect subsidies. This is why we do not invest in publicly traded companies that depend on government subsidies to make a profit (except for defense contractors).

- You work for a company that depends on a free flow of international trade. Import-export businesses, freight brokers, etc. Trump and Biden will most likely have very different trade policies. For example, Biden has kept the door more open with China (except for electric cars) and Trump has historically been more hostile from a trade perspective. But it’s not just China. Mexico, Europe, Japan, etc. all have their own trade agreements which are either “Republican-friendly” or “Democrat-friendly.”

Note that the categories of people noted above are employees and not investors, because we have noted in past updates that the stock market performs about the same, regardless of who is in the Oval Office. It doesn’t seem to make sense, but the historical data is very clear. Microsoft is going to keep selling Excel, NVIDIA is going to sell graphics chips to write term papers, Ford is going to sell cars and trucks. CEOs of publicly traded companies are tasked with making as much money as possible for shareholders, and “but [fill in the blank] is the President” is no excuse if the company’s profits fall. They adapt with the times.

So, as we say at the end of almost every update, our best advice is to build a sound financial plan based on long-term returns of a diversified investment portfolio and realistic spending goals and stick with the plan, making small course corrections along the way. It doesn’t take a server farm full of NVIDIA chips to build a plan, so don’t worry as much about what’s going to happen next quarter or next year or what the Fed is going to do or who is President. Just make sure you stay on the long-term path.

Hopefully we will make it through the Summer without melting, and we will be back with another update in early October (a month before the election!) Please contact us if you have any questions.