2024 Q4 Review and Outlook – The Stopped Clocks Start Chiming

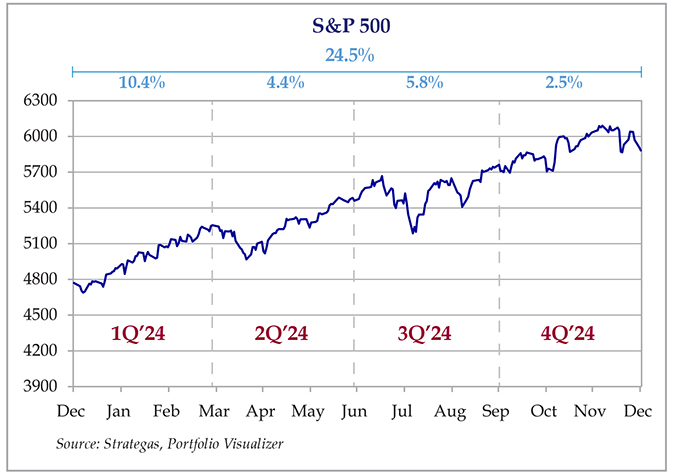

Markets recorded a fabulous 2024 as stocks (as measured by the S&P 500 SPDR ETF – SPY) gained 24.5%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 0.7%, and a 60% stock/40% bond portfolio recorded a 15% total return. The last decade was equally impressive as stocks earned a 13% compounded annual return, bonds 1.3% and a 60/40 portfolio (rebalanced annually) grew 8.4% per year from 2014 to 2024.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

The Stopped Clocks Start Chiming

We hope everyone enjoyed the holiday season. One “holiday” that Wall Street celebrates is the annual forecast derby conducted by economists and strategists at investment banks, brokerage houses and money managers all over the world. Accordingly, here is our forecast:

“With relatively little fanfare, the stock market has become expensive again. While the rest of economy has been growing frustratingly slowly for almost five years, stocks have been rising at a boomlike clip.

Relative to long-term corporate earnings…stocks have been more expensive only three times over the past century than they are today, according to data from Robert Shiller, a Nobel laureate in economics. Those other three periods are not exactly reassuring, either: the 1920s, the late 1990s and in the prelude to the 2007 financial crisis.”

Actually, that ISN’T our forecast– it is a slightly edited version of an article in the New York Times written by financial journalist David Leonhardt…in 2014. At the time of publicatiwww.nytimes.com/2014/05/06/upshot/time-to-worry-about-stock-market-bubbles.html#on, the S&P 500 index was about 1,850. It is now above 5,900.

Mr. Leonhardt has had a decent reputation as a journalist over the years, and the full article took a measured tone. In fact, he stated quite clearly further down the page that “I’m not predicting that the market is going to fall 12 percent or 50 percent. (And if I did, you should stop reading this column.)” However, many readers may have read this article and changed their investment plan to a much more conservative version (relative to what their financial plan supported) and left a lot of money on the table.

The bad news is that, for every forecast that sticks to broad concepts and takes a data-driven, thoughtful approach, there are many others (from people with financial qualifications far higher than a journalist’s) that are, to use a modern term, clickbait. And it’s a shame, because their status carries a lot of respect, and they get a lot of airtime on the major financial news outlets. CNBC is notorious for bringing in “strategists” who make outlandish claims to draw in viewers.

An example of a respected Wall Street forecaster who has occasionally made outlandish forecasts is Gary Shilling. Mr. Shilling runs an economic consulting firm and has been in the business for decades. He is credited as one of the few economists who predicted the 2008-2009 financial crisis. That being said, here is a statement he made in early 2013 – “With a global recession depressing corporate revenues, unsustainable profit margins and currency translation losses spawned by a robust dollar, I see S&P 500 operating earnings of $80 per share next year. That’s a quarter below Wall Street consensus. Throw in a bear market P/E low of 10 and the S&P 500 Index drops to 800, a 42% decline.”

There was not a 42% decline in 2013. In fact, the S&P 500 rose 32% in 2013.

And we don’t want to single him out, either. He’s a smart guy who has undoubtedly been “right” from time to time. There are investors with amazing track records who have made equally extreme statements, (e.g., Jeremy Grantham or Stanley Druckenmiller) and were proven wrong. And sometimes, they were “right,” but the market didn’t prove them right for several more years. And finally, they can change their minds on a dime. The problem is that they don’t always go back on CNBC when they shift from bearish back to bullish.

But the worst of the worst make the same catastrophic predictions every year, to sell their books and financial workshops and gold coin/cryptocurrency investments. People like Harry Dent or Robert Kiyosaki. Between 2009 and 2016, Mr. Dent wrote at least four books with the theme of an imminent market crash. The one written in 2009 – right as the market bottomed out – is titled The Great Depression Ahead. Ironically, the last time he was bullish was 1998, which was the beginning of the end of the tech boom. Mr. Kiyosaki is known for his “Rich Dad Poor Dad” series of real estate investing books and (very expensive) courses and has since “diversified” into calling for stock market crashes every month.

And now we have the “Tik Tok investors,” who make even more outlandish statements to promote their sketchy cryptocurrencies.

There is a method to their madness. All they must do is get it right one time, and they can milk it for another 10 years. The incorrect calls get lost in the noise.

You can laugh at the more flamboyant examples, but not everyone does, and too many people have made ill-advised investment decisions inspired by statements from smart, accomplished people who are unfortunately playing a different game.

There is an often-used phrase in the investment world – “Even a stopped clock tells the correct time twice a day,” and the stopped clocks are chiming.

We aren’t clocks (working or broken), so, as usual, we won’t be making a 2025 S&P 500 forecast. Stocks are long-term investments, and trying to surf the waves year to year makes no sense. If your financial plan depends on an accurate 12-month forecast for the stock market, then you have too much of your money in stocks. If your financial plan will be wrecked by a 30% drop in the stock market next year, you also have too much invested in stocks. We aren’t saying that the stock market will drop 30% in 2025 (or rise 25%) – just that it is unpredictable.

For what it’s worth, our long-term (10 year plus) outlook for stock market returns remains a bit below the historical average (7%-8% per year vs. 9%-12% historical returns). That may lead to a slightly more conservative asset allocation in some financial plans (e.g., a new retiree with few other income sources) but no change to others (e.g., a 25-year-old who is contributing every month to their 401(k)). It all depends on the needs of the financial plan.

Inflation Grinding Lower

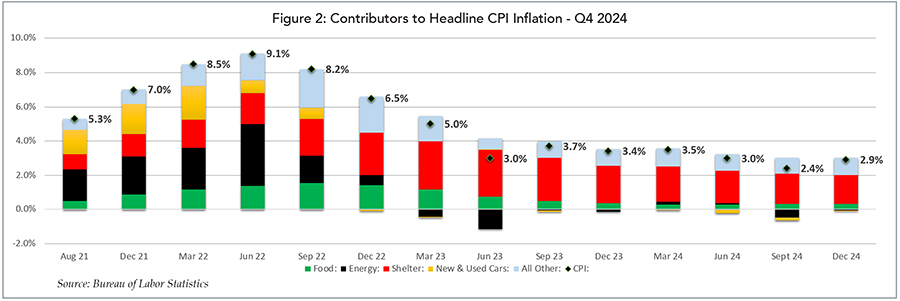

The latest inflation report was encouraging, although there is still a long road to the 2% goal. As Figure 2 shows below, the CPI index ticked up to 2.9% from 2.4% in September. However, the more stable “Core” (i.e., minus food and energy) inflation ticked down to 3.2% from 3.3%. Shelter inflation has been the most stubborn measure, and it contributed 1.7 points to the 3.2%, which represents a continuation of a very gradual downward trend from shelter’s almost 3 points of contribution to inflation in March 2023.

As encouraging as the report was, it will continue to be a grind. Just like weight loss or becoming good at chess or tennis, big improvements come early, but you really have to buckle down when the plateau hits. This plateau could last for a while, as the remaining “gains” will be more related to supply/demand issues. Apartments and houses aren’t built overnight, and the low unemployment rate will continue to maintain demand for housing.

What policymakers are most worried about is the easiest cure for inflation – a recession. Recessions are the “starvation diets” of inflation. Like bodyweight on an 800 calorie per day diet, high prices just melt away when no one has any money to buy anything. No one wants inflation, but no one likes a recession (except maybe Harry Dent).

This is the primary reason why the Federal Reserve Open Market Committee (FOMC) has started to cut interest rates – even with Core Inflation still in the 3% range. Chairman Jerome Powell believes that we can thread the needle by slowly cutting rates to maintain a bit of stimulus but still keeping them well above zero.

The other (perhaps larger) lever to pull is “fiscal” policy – government spending and taxation. We just inaugurated a new President, and he has some big ideas. Tariffs, cutting government waste, income tax cuts, and buying Greenland (and maybe Canada). Government spending is a huge driver of the economy, and trade policy could also have a large effect. Tariffs could raise prices overnight but could also reduce demand if people balk at higher prices (which may mitigate price increases). Large cuts to government spending would be very damaging to the economy in the short-term but could possibly set us up for longer-term prosperity by reducing the national debt. It remains to be seen, however, what could realistically be cut since the two largest federal budget items are Social Security and Medicare.

Figure 2: Contributors to Headline CPI Inflation

What We Are Watching

Although we don’t try to predict something as chaotic as stock prices over a one-year period, we certainly do keep an eye on the world economy and watch for key trends. Here is a sampling of some key forces driving the start of 2025.

The Fed – As we mentioned above, the FOMC will most likely continue to cut rates in 2025 but may go slower or faster than expected – it depends on the competing forces of inflation and economic growth. Current forecasts call for one or two 25 basis point (0.25%) cuts, but it could easily change to zero cuts with a resurgence of inflation, or three to four cuts should the economy weaken significantly. Both the stock and bond markets are very sensitive to any movement by the Fed, which could result in market volatility the week of each Fed meeting.

Trump’s first 90 days – Every new President attempts to charge out of the gate, and the first 90 days is the critical time to get the ball rolling on his top priorities, since the mood is generally optimistic and Congress tends to provide a bit more support. As far as market-moving policies go, tariffs have the most potential to affect the economy (good or bad) as they would have an immediate impact on prices. A hard stance on immigration would also have a potential impact on wages and labor supply, and the dark horse is the “DOGE,” Elon Musk’s government waste SWAT team. There is a very wide range of potential outcomes of this program. Less government spending is restrictive to economic growth in the short-term, but it is hard to tell how much cutting DOGE can make.

The AI Boom – A.I. dominated the investing zeitgeist in 2024, and 2025 will be a key test for the stocks receiving the largest share of the benefits such as NVIDIA, Broadcom, Microsoft, the data center builders and even the normally boring utility stocks. Valuations have jumped ahead of profit growth for these “pick and shovel” suppliers, but the profit growth in both percentage and sheer dollar terms has been breathtaking, with no immediate end in sight. With expectations this high, however, all it takes is growth to fall slightly short of inflated expectations and we could see a repeat of 2022. On the other hand, this could be just the beginning of a seismic wave of growth which clears even the highest bar. Thankfully, we own many of the beneficiaries of AI in our clients’ portfolios, but we also own a lot of other high-quality stocks that have very little to do with AI.

Geopolitics – This is related to but not entirely driven by Trump’s first 90 days, as other countries have their own agendas. China’s economy is looking shaky, and punitive tariffs could damage it further. When economies go bad, a lot of leaders will bang the war drums to take the people’s mind off the unemployment rate. In China’s case, that would mean a) more saber-rattling over Taiwan (which manufactures the majority of the world’s semiconductors) and/or b) using alliances with bad actors (e.g., Russia) to further their goals by more indirect means. Speaking of Russia, the war in Ukraine is far from over and both sides are becoming more desperate. Then there’s Palestine and Syria, and so on and so on. The “big stuff” that hits the world usually comes as a surprise, which makes forecasting the short-term direction of economic growth extremely difficult.

As usual, having the appropriate mix of stocks and bonds in your portfolio that support your long-term financial plan (which also includes prudent spending assumptions) is 90% of the battle in ensuring you weather the inevitable market downturns along the way.

Try to stay warm this season and we will return with our 1Q review when the flowers start blooming in April. Please contact us if you have any questions.