The Fed Finally Cuts

By Doug Mewhirter

Senior Vice President – Portfolio Manager

On September 19th the Federal Reserve Open Market Committee (FOMC) voted to reduce the target interest rate by 50 basis points (a half of a percentage point). Although a rate cut was almost guaranteed, there was a lot of discussion and debate on the financial news and social media whether the Fed would cut 25 basis points (bps) or 50 bps, which conveniently filled about two weeks’ worth of financial news airtime. CNBC owes the Federal Reserve about half its annual profits.

In the financial world, there is no more scrutinized organization than the FOMC. Analysts, economists and news reporters parse every single word uttered by Chairman Jerome Powell and the Board of Governors for clues as to their future intentions. When we say “every single word,” we mean it – there are organizations that will compile side by side comparisons of Chairman Powell’s current remarks with his previous remarks, highlighting the change of an “and” to an “or,” or “strong growth” to “strong but moderating growth.” Who said there aren’t any career opportunities for English majors anymore?

Does any of this matter? Yes, but not in the way the financial pundits spin it. The Federal Reserve is one of the most powerful financial institutions in the world, and its actions influence the interest rates people pay for loans and receive on savings accounts – especially shorter-term loans and savings. Many loans are tied to benchmarks such as the Prime Rate. The Prime Rate is in turn directly affected by the Federal Reserve’s target rate. So, if you are shopping for a car and the best deal on a 5-year loan has been 6%, it might be worth checking again in a week if you are serious about buying a car – you might get 5.5% or even 5%. On the other hand, money market accounts will be paying you less interest, which means you may have to shop around if you need to carry a large cash balance for an extended period (e.g., an “emergency fund” of 6-12 months of spending).

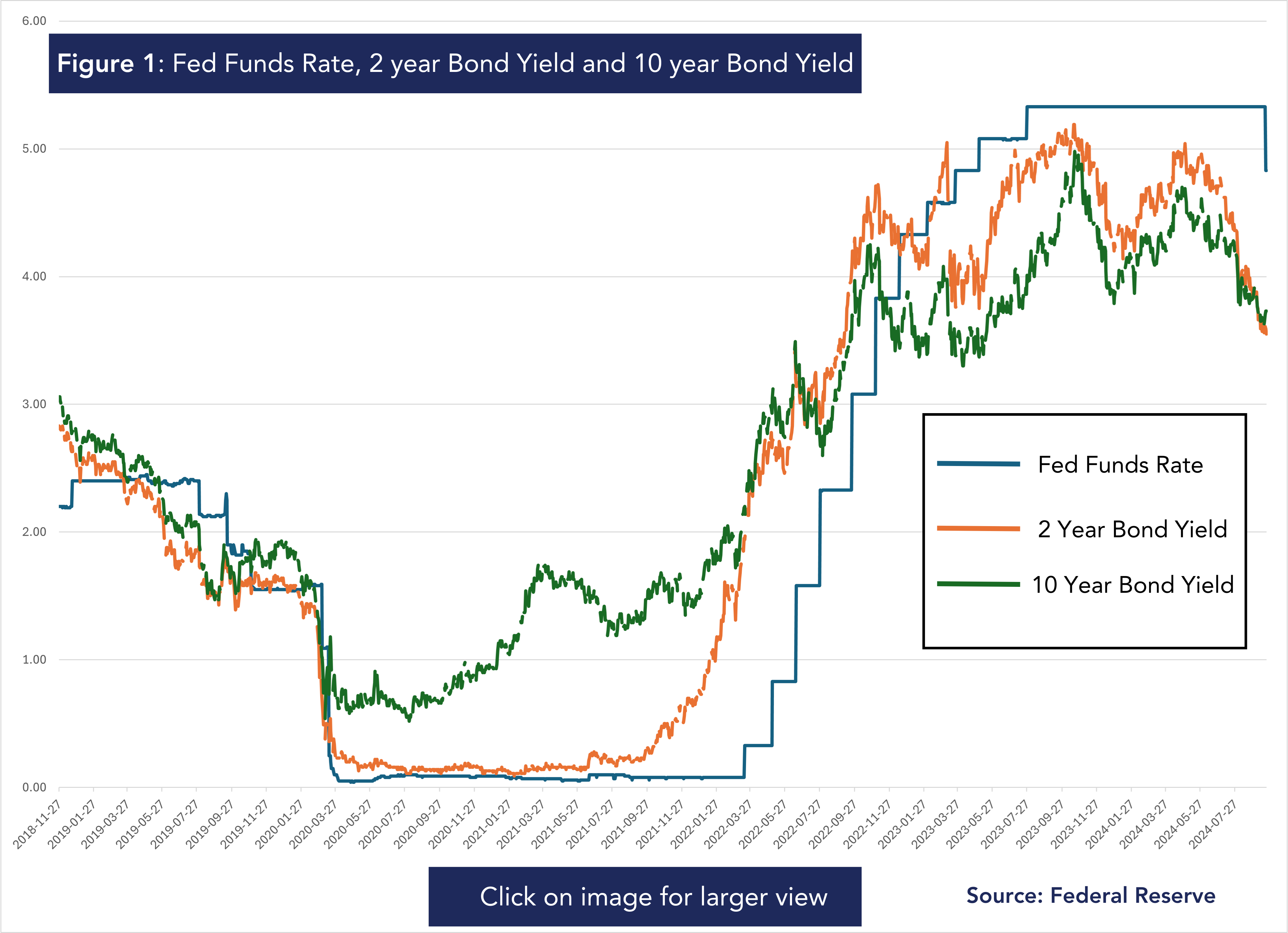

Longer-term loans such as mortgages may also get cheaper, although the Federal Reserve does not directly control those rates. The bond market reacts to the changes in the short-term rates, but also considers longer-term and less predictable factors such as future economic growth and inflation. In fact, on the day that the rate cut was announced, intermediate and long-term bond yields hardly moved. As Figure 1 shows below, rates had already come down in anticipation of rate cuts as well as moderating inflation and economic growth forecasts.

What is also worth considering is the reasoning behind the rate cuts. Lower interest rates generally stimulate the economy. Lower interest car loans make cars more affordable and increase demand. Lower mortgage rates increase demand for houses. In addition, lower interest rates on savings accounts push account holders to seek out higher returns in riskier assets (stocks and bonds) which could increase demand for stocks and bonds. However, this increased demand also increases the risk of inflation – and inflation is probably the most significant economic factor for the general public (as well as an election hot button issue).

So, if inflation hasn’t quite reached the Federal Reserve’s target of 2.0%, why are they cutting interest rates? Mr. Powell believes (and most of the data shows) that economic growth is slowing, and the risks of the U.S. slipping into a recession outweigh the inflation risks. Mr. Powell and company are trying to walk a very fine line of supporting a slowing economy without re-igniting inflation, and unemployment has been ticking up (albeit from extremely low levels) and some factors such as industrial production and retail sales have moderated.

What should you not worry about? Whether or not to sell or buy stocks or bonds, or drastically change your investment portfolio (which is what most of the financial community wants you to worry about). The stock and bond markets (which, again, are not controlled by the FOMC) are pretty smart, and constantly look toward the future. Once the FOMC acts, the markets have already adjusted (take another look at Figure 1). This doesn’t mean that there won’t be volatility – just that the direction of that volatility is unpredictable. People who try to manage their portfolios to every utterance of Mr. Powell wind up chasing their tails. Stocks are best used as long-term investment vehicles, not Beanie Babies. We have no idea if stocks will rise or fall next year, but, based on history, a high-quality stock portfolio should be much more valuable 10 to 20 years from now.

But, if you are still worried about your portfolio, J.P. Morgan Asset Management looked back at past rate cut cycles, and the results imply better than average prospects for both stocks and bonds (with no guarantees!):

Stocks and bonds tend to do well.

-

- Stocks: Since 1980, five of the 10 best years for the S&P 500 happened when the Fed was cutting rates without a recession (1985, 1989, 1995, 1998, 2019). The Fed has cut rates 12 times when the S&P 500 was within 1% of its all-time high. The market was higher one year later all 12 times (with a median return of 15%).

- Bonds: Since 1970, high-quality bonds have outperformed cash by an average of 10% in cutting cycles.

Source: J.P. Morgan Asset Management

In summary, this is what you should be doing after this rate cut (in rough order of importance):

- Once the dust has settled, double-check the rate you are earning in your savings accounts, and see if there are any higher rate options.

- If you are in the market for a car or a house but have been put off by high loan rates, go back and check to see if rates have come down – you might be pleasantly surprised.

- For those who are employed, take the temperature of your current organization – has business slowed down? If so, you might want to ensure that your emergency fund (6-12 months of household spending) is topped up.

This is what you shouldn’t be doing:

- Making drastic changes to your investment portfolio.

- Worrying if Jerome Powell says “moderate growth” instead of “growth” at his next speech.

We didn’t run off to trade stocks when the rate cut was announced, and neither should you. There will be many, many rate increases and decreases over the next 10-20 years, so obsessing about each one will just unnecessarily increase your stress levels and derail your financial plan.

Please contact us if you have any questions and enjoy watching the leaves turn!