2024 Q3 Review and Outlook – The Fed Cuts, the Election Looms

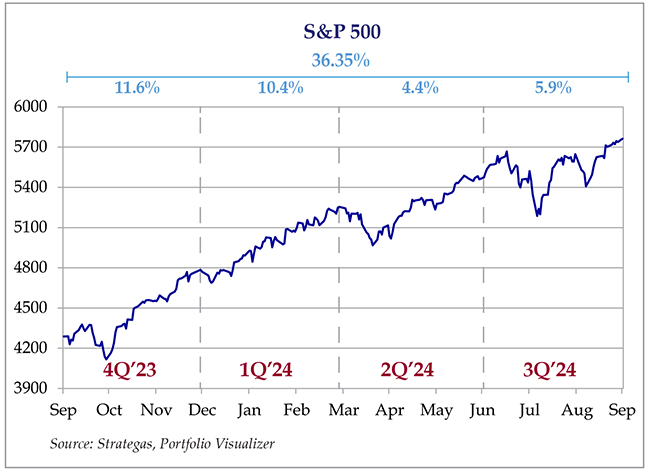

Markets continued to rise in the third quarter as stocks (as measured by the S&P 500 SPDR ETF – SPY) gained 5.8%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 5.3%, and a 60% stock/40% bond portfolio recorded a 5.6% total return. Year to date, stocks returned 21.9%, bonds 4.5% and a 60/40 portfolio 14.9%, which brings us to the end of the year with a lot of momentum.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

The Fed Finally Cuts

Editor’s Note: This section was a standalone article published on our website and our Fall 2024 E-Newsletter.

On September 19th the Federal Reserve Open Market Committee (FOMC) voted to reduce the target interest rate by 50 basis points (a half of a percentage point). Although a rate cut was almost guaranteed, there was a lot of discussion and debate on the financial news and social media whether the Fed would cut 25 basis points (bps) or 50 bps, which conveniently filled about two weeks’ worth of financial news airtime. CNBC owes the Federal Reserve about half its annual profits.

In the financial world, there is no more scrutinized organization than the FOMC. Analysts, economists and news reporters parse every single word uttered by Chairman Jerome Powell and the Board of Governors for clues as to their future intentions. When we say “every single word,” we mean it – there are organizations that will compile side by side comparisons of Chairman Powell’s current remarks with his previous remarks, highlighting the change of an “and” to an “or,” or “strong growth” to “strong but moderating growth.” Who said there aren’t any career opportunities for English majors anymore?

Does any of this matter? Yes, but not in the way the financial pundits spin it. The Federal Reserve is one of the most powerful financial institutions in the world, and its actions influence the interest rates people pay for loans and receive on savings accounts – especially shorter-term loans and savings. Many loans are tied to benchmarks such as the Prime Rate. The Prime Rate is in turn directly affected by the Federal Reserve’s target rate. So, if you are shopping for a car and the best deal on a 5-year loan has been 6%, it might be worth checking again if you are serious about buying a car – you might get 5.5% or even 5%. On the other hand, money market accounts will be paying less interest, which means you may have to shop around if you need to carry a large cash balance for an extended period (e.g., an “emergency fund” of 6-12 months of spending).

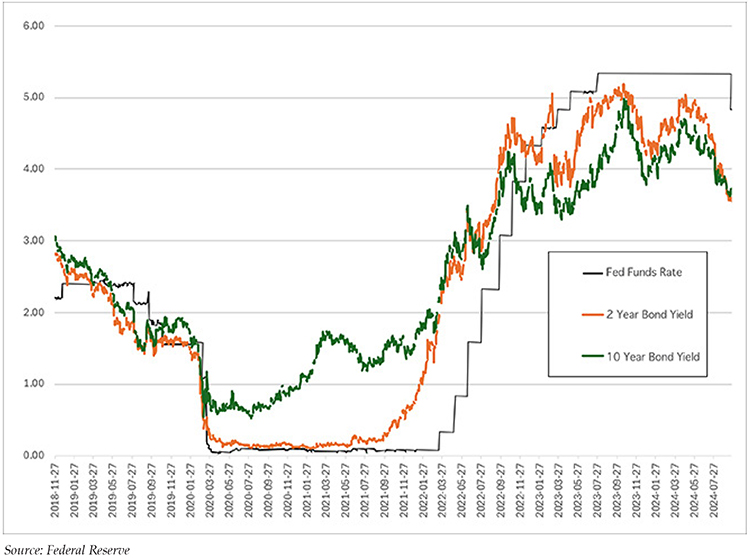

Longer-term loans such as mortgages may also get cheaper, although the Federal Reserve does not directly control those rates. The bond market reacts to the changes in the short-term rates, but also considers longer-term and less predictable factors such as future economic growth and inflation. In fact, on the day that the rate cut was announced, intermediate and long-term bond yields hardly moved. As Figure 2 shows below, rates had already come down in anticipation of rate cuts as well as moderating inflation and economic growth forecasts.

Figure 2: Fed Funds Rate, 2 year Bond Yield and 10 year Bond Yield

What is also worth considering is the reasoning behind the rate cuts. Lower interest rates generally stimulate the economy. Lower interest car loans make cars more affordable and increase demand. Lower mortgage rates increase demand for houses. In addition, lower interest rates on savings accounts push account holders to seek out higher returns in riskier assets (stocks and bonds) which could increase demand for stocks and bonds. However, this increased demand also increases the risk of inflation – and inflation is probably the most significant economic factor for the general public (as well as an election hot button issue).

So, if inflation hasn’t quite reached the Federal Reserve’s target of 2.0%, why are they cutting interest rates? Mr. Powell believes (and most of the data shows) that economic growth is slowing, and the risks of the U.S. slipping into a recession outweigh the inflation risks. Mr. Powell and company are trying to walk a very fine line of supporting a slowing economy without re-igniting inflation, and unemployment has been ticking up (albeit from extremely low levels) and some factors such as industrial production and retail sales have moderated.

What should you not worry about? Whether or not to sell or buy stocks or bonds, or drastically change your investment portfolio (which is what most of the financial community wants you to worry about). The stock and bond markets (which, again, are not controlled by the FOMC) are pretty smart, and constantly look toward the future. Once the FOMC acts, the markets have already adjusted (take another look at Figure 1). This doesn’t mean that there won’t be volatility – just that the direction of that volatility is unpredictable. People who try to manage their portfolios to every utterance of Mr. Powell wind up chasing their tails. Stocks are best used as long-term investment vehicles, not Beanie Babies. We have no idea if stocks will rise or fall next year, but, based on history, a high-quality stock portfolio should be much more valuable 10 to 20 years from now.

But, if you are still worried about your portfolio, J.P. Morgan Asset Management looked back at past rate cut cycles, and the results imply better than average prospects for both stocks and bonds (with no guarantees!):

“Stocks and bonds tend to do well.

- Stocks: Since 1980, five of the 10 best years for the S&P 500 happened when the Fed was cutting rates without a recession (1985, 1989, 1995, 1998, 2019). The Fed has cut rates 12 times when the S&P 500 was within 1% of its all-time high. The market was higher one year later all 12 times (with a median return of 15%).

- Bonds: Since 1970, high-quality bonds have outperformed cash by an average of 10% in cutting cycles.”

Source: J.P. Morgan Asset Management

In summary, this is what you should be doing after this rate cut (in rough order of importance):

- Once the dust has settled, double-check the rate you are earning in your savings accounts, and see if there are any higher rate options.

- If you are in the market for a car or a house but have been put off by high loan rates, go back and check to see if rates have come down – you might be pleasantly surprised.

- For those who are employed, take the temperature of your current organization – has business slowed down? If so, you might want to ensure that your emergency fund (6-12 months of household spending) is topped up.

This is what you shouldn’t be doing:

- Making drastic changes to your investment portfolio.

- Worrying if Jerome Powell says “moderate growth” instead of “growth” at his next speech.

We didn’t run off to trade stocks when the rate cut was announced, and neither should you. There will be many, many rate increases and decreases over the next 10-20 years, so obsessing about each one will just unnecessarily increase your stress levels and derail your financial plan.

Inflation Meandering Closer to Target

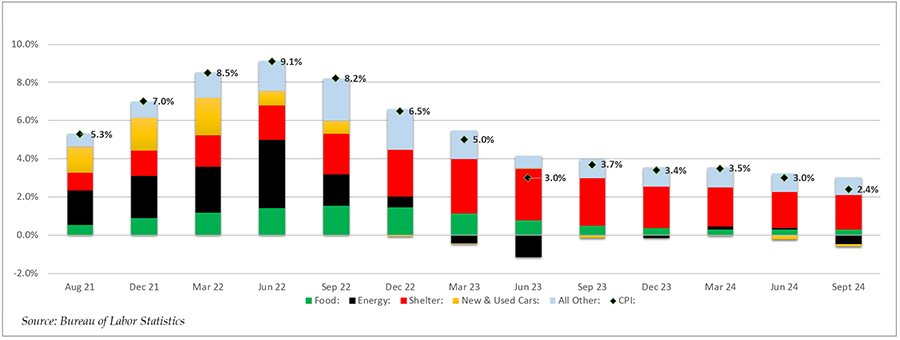

The latest inflation report was a mixed bag. As Figure 3 shows below, the CPI index increased only 2.4% in September vs. September last year, but the Core CPI increased 3.3% as energy prices (which aren’t in the Core) reduced the CPI by a half of a percentage point. (You may have noticed that gasoline prices briefly went under $3.00 a gallon for a brief moment.) Also, both the “headline” and the Core CPI were slightly higher than expectations, which caused some concern from economists.

There were some bright spots. Shelter inflation continues to moderate, contributing 1.8 percentage points to the CPI. This is the lowest contribution since June 2022. Also, new and used car prices fell again as supply and demand have finally come back into some sort of balance.

The Federal Reserve Board also seems more comfortable with the inflation picture, based on the recently released minutes of the FOMC’s September meeting, with one quote stating “with regard to the outlook for inflation, almost all participants indicated they had gained greater confidence that inflation was moving sustainably toward 2 percent.”

There were also concerns about a tight labor market, which provides fuel for long-term inflation as people demand higher raises in response to higher prices, which leads to more spending which leads to even higher prices, and so on… However, the Fed governors’ fears seem to have eased a bit, as “participants noted that labor market conditions had eased further in recent months and that, after being overheated in recent years, the labor market was now less tight than it had been just before the pandemic.” (emphasis ours).

While the path to 2% has become longer than we want, we believe that the Fed’s overall policy of slowly easing rates will not materially change. The next meeting could still produce another 25 basis point cut, with the latest inflation report just taking 50 bps off the table and the chances of a “pause” slightly higher.

Figure 3: Contributors to Headline CPI Inflation

The Election

The election is looming – only one more month of calls/texts/TV commercials/smoke signals/carrier pigeon messages to endure! We have spilled a lot of ink over the past year warning investors not to do anything foolish from an investment perspective in the weeks leading up to and immediately following the election. We do encourage – in the strongest way – all of you to vote. While participating in the political process is vital to the long-term health of our democracy, making drastic financial changes in response to the “wrong” election winner can be very detrimental to the long-term health of your finances.

Let’s presume that you have heeded our warnings about staying disciplined through the inevitable craziness of the election period (which will most likely bring a lot of short-term volatility to the financial markets) but you couldn’t resist reading CNBC’s latest article “Five Key Moves to Make Ahead of the Election to Turbocharge your Portfolio!” and you want to make some “adjustments.” A lot of these adjustments involve buying or selling specific sectors in response to a liberal or conservative President-Elect. Some of these adjustments make logical sense. However, history shows that the investment results can often go in the opposite direction.

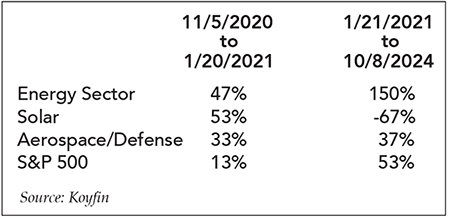

The most recent example is the 2020 election. Joe Biden’s tree-hugging administration’s environmental policy is very supportive of renewable energy (particularly solar) and less friendly to fossil fuels (particularly oil). Therefore, you should have bought solar companies and sold oil companies after he was sworn into office. For good measure, sell the defense companies, because “Democrats want to cut the defense budget.” Looking at the next table shows what a horrible decision that would have been:

Figure 4: Performance of Selected Sector ETFs, 2020 Election to Inauguration and Inauguration to Present

Although everything rallied from Election Day to Biden’s inauguration as the uncertainty surrounding the election slowly receded, Biden’s term to date showed a wide deviation between “clean” and “dirty” energy stocks, with the Energy Sector SPDR (XLE) rising 150% since 1/21/2021 and Invesco Solar ETF (TAN) investors losing two-thirds of their original investment. Meanwhile, the S&P 500 rose 53% and the Aerospace and Defense ETF (XAR) returned 37% – lower than the S&P but still a healthy gain.

That doesn’t mean you should just do the opposite of the obvious investment either. Sometimes the “logical” decision works – but it works or doesn’t work due to a host of complicated economic, political, investment and business factors, some of which are not known prior to the election.

So please, try to stay away from “adjustments” or “tweaks” to your portfolio based on political outcomes. You may as well go to a casino and put your portfolio on a roulette table. There may be a case for one stock or sector vs. another stock or sector based on the political climate, but politics is only one of many factors that need to be considered in the decision.

So, as we say at the end of almost every update, our best advice is to build a sound financial plan based on long-term returns of a diversified investment portfolio and realistic spending goals and stick with the plan, making small course corrections along the way. Long-term clients of TCV Trust & Wealth Management have been rewarded by our steady approach to investing over the years. Our firm and clients have seen many market ups and downs, and will see many more, but sticking to sound financial plan will help weather any economic storms…sometimes even a hurricane.

Enjoy the crisp Fall weather and the changing leaves, and we will return in January for the year-end review. Please contact us if you have any questions.