2025 Q1 Review and Outlook – The Tariff Tantrum

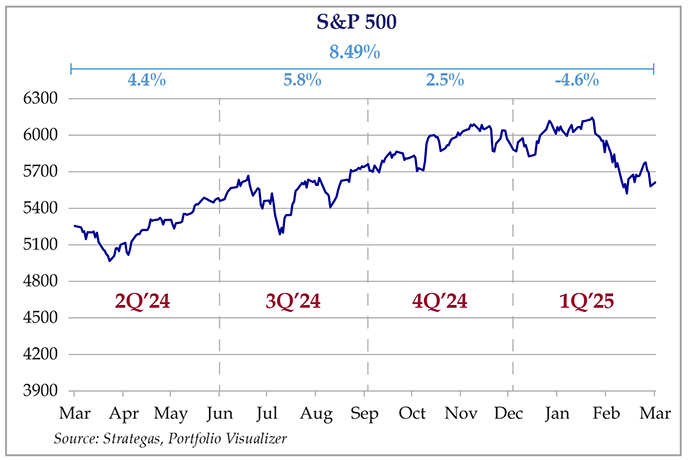

The market stumbled out of the gate in 2025 as stocks (as measured by the S&P 500 SPDR ETF – SPY) fell 4.6% during the first quarter. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 2.4%, and a 60% stock/40% bond portfolio declined 1.8%. In April, stocks fell an additional 11% before recovering about half of that loss as of April 16th.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

The Tariff Tantrum

Welcome to 2025! Please ensure your seatbelts are fastened, as we have encountered some turbulence. We can expect the turbulence to continue for a while. How long is “a while?” We don’t know, and that’s the root of the problem. The Trump administration’s proposed trade policies (i.e. tariffs) have been – to put it lightly – disruptive, and they change literally every day.

The market is not wildly bouncing around because investors are running a detailed analysis of economic impacts and adjusting corporate profit forecasts, it is volatile due to uncertainty. Nobody can see the endgame to these pronouncements. First it was targeted tariffs on our biggest trading partners, then “reciprocal”

tariffs (which implies that the rates are matched) then large worldwide tariffs which are based on trade deficit calculations. The most recent headlines are now focusing on a 104% tariff on China (breaking update – 125%) and a retaliatory 81% tariff on the U.S. by China. Tomorrow will most likely be something different, as trade negotiators are busy talking to over 70 countries, and industry lobbyists are furiously pushing for exceptions.

The stock market abhors uncertainty. Since the exact future is unknowable, investors try to narrow their forecasts down to a handful of scenarios. In calmer times, things look much simpler – just take last year’s growth and project it out a few more years. When chaos reigns, the scenarios multiply like rabbits, and investors demand a wider margin of safety. This often causes the across-the-board selloffs that we experienced in the first week of April as investors “sell first, ask questions later.” With all that said, we’ll attempt to break down the whats and the hows and the whys of tariffs, and give our best guess of bullish, midrange and bearish scenarios (which are, needless to say, subject to change without notice.)

The What and the How

Tariffs are one of the oldest systems of government revenue generation, and recently the most controversial. It is a tax charged to an importer of goods or services that are manufactured in a targeted country. Note that the importer pays the tax, not the exporter.

For example, Apple builds iPhones in various overseas countries (mainly China and Southeast Asia) via an outsourced manufacturing company such as Foxconn. Under a zero-tariff system, Foxconn builds the iPhone and charges Apple, say, $400 for every iPhone delivered to Apple’s domestic warehouses. Apple then sells them to Verizon and T-Mobile at a marked-up price (maybe $700) which is then marked up again to $900-$1000 to the retail customer. If there is a 50% tariff, then Apple pays $400 for the iPhone, plus an additional $200 to the U.S. government (50% of $400), so its total cost is now $600. Apple now has a decision to make.

The company can:

1. Eat the tariff and reduce its profit margin. This would put a huge dent in Apple’s profits.

2. Add the $200 tariff to the wholesale price of the iPhone. This could reduce demand for the product and contribute to inflation.

3. Go back to Foxconn and try to get them to lower the wholesale price of the iPhone. Foxconn runs on slim margins (it relies on huge volume for their profits) so it doesn’t have a lot of wiggle room. This may also cause Foxconn to cut corners and hurt the product’s quality.

4. Build an iPhone factory (or have Foxconn build a factory) in the U.S. to avoid the tariff. This a) solves the tariff problem and b) increases investment in the U.S. (and reduces it in a rival such as China). However, there is no way that iPhones can be made for $400 in the U.S. (which is why they are made overseas in the first place). If a U.S.-made iPhone costs $600, then Apple still gets squeezed and must either sacrifice its profit margin or raise the price of the iPhone.

5. A little of everything. Apple moves the production of certain components onshore, moves other factories to countries with lower tariffs, eats some of the tariff and passes the remainder of the increased cost to the consumer.

Now, repeat this process with every company that imports products from every other country in the world. Walmart and Amazon stock prices have been particularly volatile due to their reliance on imports, slim profit margins and low prices that are difficult to pass on to customers. Auto companies (which also have low margins) have incredibly complex supply chains that may involve parts and finished products crossing multiple borders.

As if this didn’t cloud our crystal balls enough, tariffs create economic effects that have a long-term impact on the world economy.

Some of these effects include:

1. Inflation. If Walmart pays a 50% tariff on a Chinese-made toy that it buys for $10 and sells for $15 (by buying for $10, paying the U.S. $5 and selling for $20) then prices increase 33% (a $5 price increase on a $15 toy). Although imports are only 15% of our economy, those 33% increases would add up and put pressure on inflation. This has been the primary concern raised by economists.

2. Currency changes. Let’s say Apple moves some production onshore and moves other factories to lower tariff countries. We won’t buy as much of the target country’s currency as before, which would weaken it relative to the dollar. If it weakens enough, then it will offset some or all of the tariff. If Foxconn’s dollar cost to make an iPhone drops from $400 to $300 due to China’s currency depreciation, then Apple has $100 of additional wiggle room, which would cause Apple to move less production onshore.

3. Shifting trade patterns. Since tariffs aren’t uniform worldwide, production sources would move to the countries with the combination of lowest cost and lowest tariffs, which would then require another round of adjustments and negotiations. For example, if Vietnam negotiates a low tariff (in exchange for favorable terms to the U.S.), a Chinese company could set up a Vietnamese subsidiary which receives the product from China, then immediately ships it to the U.S. under the lower Vietnamese tariff rate. The U.S. would need to demand that these “pass through” companies be prohibited in Vietnam.

4. Actual tariffs collected will differ from expected. The combined effects of #1-#3 will result in fluctuating tariff collections. If production moves onshore, tariff revenues drop. If foreign currencies weaken, tariffs drop. If production moves around, tariffs may rise or fall, depending on volumes and currencies, etc.

If you notice that this is complicated, you aren’t alone. This is why almost all economists believe tariffs are a drag on economic growth. That extra $200 per iPhone creates a “deadweight loss” that is hard to recover.

But, tariffs aren’t implemented solely for economic reasons.

The Why

This part veers dangerously close to a political discussion, so we will attempt to be as objective as possible. While we don’t know exactly why the Trump administration is being so aggressive with tariffs, we can determine a few key reasons.

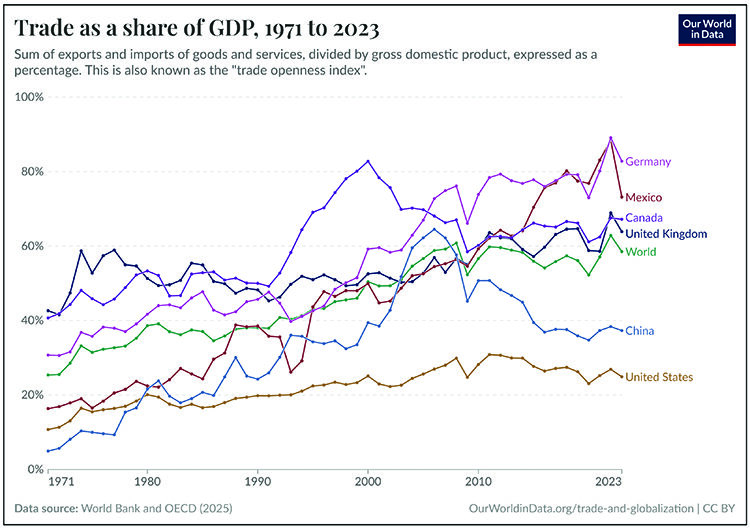

1. Geopolitics. As the Figure 2 shows (which is also in our recent article about tariffs), “the world needs us more than we need the world” (from a strictly economic point of view.) Imports are a smaller part of our economy than exports are of our trading partners’ economies. This gives us the ability to apply pressure to accomplish political goals (e.g., immigration, drug trafficking, military alliances, etc.)

2. Rebuilding the U.S.’s industrial base – especially in “strategic industries.” The loudest proponents of tariffs have criticized the long-term “hollowing out” of our industrial base. “We just push paper and build brain-rotting social media apps!” Our shipbuilding industry is kept alive solely by the military and the Jones Act, steel mills are less competitive (and it’s impossible to build a steel mill without foreign-made machinery) and the entire semiconductor industry depends on China’s unwillingness to invade Taiwan.

3. Promoting domestic employment and “good jobs.” Our unemployment rate remains very low, but critics claim it is heavily padded with low-paid, low-quality service jobs such as DoorDash drivers. Even if the pay isn’t much higher for an entry level mechanic, there may be more upside for this person’s career than waiting tables.

4. Reducing reliance on income taxes. Since tariffs are a source of revenue, it gives the administration room to cut taxes elsewhere (or, heaven forbid, pay down debt), which, in their opinion, would (in combination with #1-#3 above) provide long-term benefits that would outweigh the negative impacts of the tariffs on inflation and financial markets.

Figure 2: Trade Intensity by major country

Possible Scenarios

As we mentioned earlier in the article, the scenarios are multiplying like rabbits. We have tried to distill the many possible futures down to “bull,” “bear” and “middle of the road” scenarios. Note that “middle of the road” doesn’t mean “most likely.” It could really go in any direction (which explains the insane market volatility).

- The “bull” – the world plays ball, and all tariffs drop (along with additional concessions in our favor.) We believe that Trump and his advisors wouldn’t mind if tariffs were low – as long as we have an “even playing field.” That’s the tricky part, and countries use a lot of levers to protect their favored industries. If we are satisfied that the majority of our largest trading partners back down, then we may go back to where we were at the end of the Biden administration, only with a lot of extra factors in our favor. Since the economy was still growing in January 2025, there’s no reason it can’t continue to grow or even accelerate – with additional investment in the U.S. and a stronger overall manufacturing base.

- The “bear” – the world digs in their heels, and we get a) higher inflation and b) a slower economy (and lower than expected revenue from tariffs). Although domestic industries would increase, the new jobs would be much fewer than forecast in this bear scenario, as the shiny new U.S. factories will be run by robots. Plus, Europe and Canada could open their doors wider to China, which would weaken our geopolitical position.

- The “middle” – some countries (Trump estimates 70 countries as of today) will cut a deal, and others (such as China) will dig in their heels and/or form trade agreements away from the U.S. This may still push inflation higher, but not to the worst case scenarios. If we expect long-term inflation of 2%-3% per year, then the “new world order” CPI growth may stick to the upper end of that range. While the Fed would be less inclined to lower rates, drastic rate increases would be off the table and overall economic growth may continue at current rates. China’s economy may continue to struggle (it never fully rebounded from COVID) and, if our current trading partners are satisfied with their deals with the U.S., it wouldn’t be able to “grow around the U.S.” as much as President Xi would like.

To summarize, the bull case would see stocks and economic growth resume their upward march, with the bear case taking an opposite tack, moving close to the dreaded “stagflation” scenario (i.e., a recession with high inflation), while the middle of the road scenario would be a “muddle along” situation.

Inflation – The Calm Before the Storm?

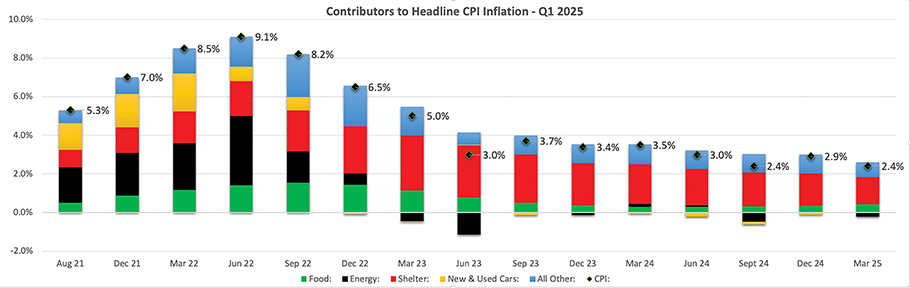

On a brighter note, the latest inflation report showed continued progress toward the Federal Reserve’s 2.0% goal. As Figure 3 shows below, the CPI index fell to 2.4% from 2.9% at the end of 2024. Furthermore, the more stable “Core” (i.e., minus food and energy) inflation ticked down to 2.8% from 3.2%. Shelter inflation has been the most stubborn measure but showed further improvement to a 1.4% contribution to CPI, down from 1.7% in December 2024 and almost 3% in March 2023.

However, all of this comes with a giant asterisk. With the world economic card table kicked over, we believe that the CPI will become more volatile should the tariffs stick at higher rates – for all the reasons we described above. This doesn’t mean that inflation will immediately skyrocket, however, and, as companies adapt their supply chains to the new world order (whatever that turns out to be), some of the negative impact could be muted. Of course, as we mentioned in our last newsletter a deep recession can also be a quick cure for inflation – but that’s like getting chemotherapy for a case of the flu.

Source: Bureau of Labor Statistics

What Can You Do?

This all sounds like a huge mess, and the uncertainty is very unsettling. This can encourage people to make rash or hasty decisions that trade short-term emotional relief for unfavorable long-term financial consequences.

Here are a few things you can do:

- Make sure that you have enough cash for any near-term (0-2 years) big ticket spending items. You don’t want your wedding fund exposed to any market volatility – especially in this environment.

- If you work for a company that could be materially impacted by tariffs, then you should ask more questions about how your employer is going to adapt (and keep your resume updated and make sure your emergency fund is topped off at 6-12 months of expenses).

- Ensure that your overall mix of stocks and bonds fits the needs of your long-term financial plan. If you are retiring next year and intend to use your portfolio for living expenses, then you probably don’t want the portfolio 100% in stocks. On the other hand, if you are 30 years old and regularly contributing to your 401(k) plan, keep investing in stocks and take advantage of the volatility!

- If you are comfortable with your current asset allocation, consider rebalancing. Most portfolios have become “stock heavy” following the last two years of spectacular returns, so trimming back your stock positions can help manage the portfolio risk. Also, if stocks plummet during 2025, then you need to consider rebalancing by buying stocks (assuming your portfolio drifts toward bonds due to the stocks dropping so much). This is very difficult to do, but potentially very good for the long-term performance of the portfolio.

- If you have a stock or mutual fund that is deep in a loss in a taxable account, consider selling it to take the tax loss (which can offset future gains). If you still like the stock, you can buy it back in 31 days. Otherwise, that may be the push you need to finally get rid of a low-quality company or underperforming mutual fund that you never got around to selling.

- No rash or hasty decisions!

Most of this advice can and should be applied at any point of the market cycle, but the current environment can help you put some extra focus on these basic steps that will ensure long-term financial success. Enjoy the flowers (and pollen!) and we will return with our 2Q review in July. Please contact us if you have any questions.